Article Introduction

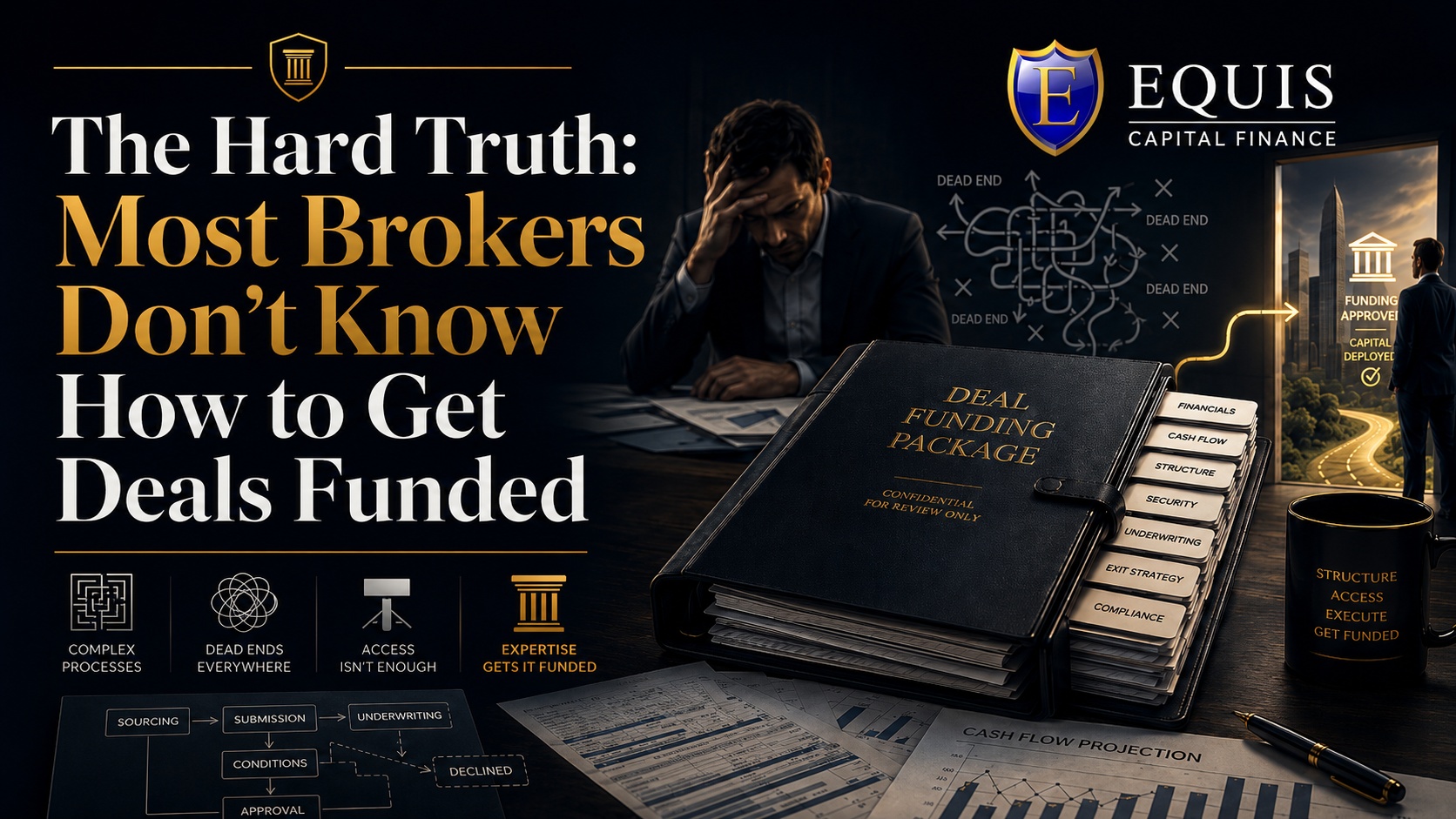

The hard truth most borrowers never hear is simple. Most commercial financing brokers do not actually know how to get deals funded. They know how to forward a package and chase calls, but that is not the same as understanding how lenders approve capital.

This hard truth explains why so many commercial real estate financing requests stall after months of noise. The broker blames the market, interest rates, or lender appetite, while the real problem sits in the file. Structure, risk, and documentation decide whether capital shows up.

In this article, we unpack why deals really fail, how lenders think, and what separates a file-circulator from a real capital advisor. The goal is blunt but practical guidance so borrowers, referral partners, and even brokers can see where execution breaks down. Keep reading if you suspect your own deal should have closed by now.

Key Takeaways

- Most failed commercial deals share the same root cause. The issue is usually not a lack of capital in Canada, but weak deal packaging, poor capital stack design, and a broker who does not understand institutional underwriting. When the file is confused, inconsistent, or incomplete, even a good opportunity looks risky.

- Shopping the deal is not the same as structuring it. Sending a loan request to more lenders without fixing the structure only multiplies rejections. Real deal funding strategies start with aligning loan sizing, collateral, equity, and exit strategy, then choosing a lender whose mandate actually fits that profile.

- Lenders evaluate risk, not enthusiasm or storytelling. Credit teams at banks and private lenders review cash flow, sponsor strength, security, debt-service coverage, and exit routes. A neat, supported package that answers those questions builds confidence quickly, while a loose story filled with gaps does the opposite.

- A broker simply introducing lenders is different from a capital advisor running lead. An advisor diagnoses the transaction, redesigns the capital stack where needed, prepares institutional-grade material, and manages the commercial loan approval process from first look to funding. That discipline determines whether a deal closes.

- Borrowers should expect upfront honesty, technical review, and targeted strategy from any serious partner. That means an initial transaction review, clear go or no-go feedback, lender matching based on mandate, and realistic timelines. Firms like Equis Capital Finance live in this advisory role rather than just brokering introductions.

The Broker Myth: Why Knowing Lenders Is Not Enough

The broker myth that a long lender contact list equals funding kills more deals than interest rates. Knowing a few people at banks or private funds is helpful, but it is not a capital strategy. The hard truth is that lender names do nothing if the transaction itself is not structured to meet credit policy.

Most commercial mortgage broker marketing leans on relationships. You hear lines about access to private lending for brokers, or how many lenders a firm can reach. That sounds comforting when a borrower is stressed. It does not answer the real question, which is how to get deals funded through underwriting, not charm.

Institutional lenders like RBC, TD, BMO, CIBC, Scotiabank, and National Bank follow detailed credit frameworks. So do private credit funds, pension funds, and debt funds. They look at leverage ratios, security, sponsor strength, sector risk, and repayment coverage. A broker who only forwards financials without understanding those drivers is guessing, not advising.

Here is where mortgage broker mistakes start to stack up:

- They send a construction deal to a lender that only wants stabilised income assets.

- They push a highly geared refinance to a bank that is tightening its real estate book.

- They ask for terms that ignore lender requirements for brokers and sponsors altogether.

According to Statistics Canada, about one in five Canadian small and medium-sized enterprises that sought external financing were turned down or only partially approved (Statistics Canada). That headline often gets blamed on tight markets. In practice, a large share of those files were never lender-ready in the first place.

Equis Capital Finance sees this pattern weekly across Canada and the United States. A broker promises that a deal is fundable, circulates a thin package, and then disappears when credit pushes back. By the time an experienced capital advisor reviews the file, the borrower is tired, deadlines are close, and lender goodwill is already damaged.

“We don’t decline good projects; we decline weak files.”

— Senior credit officer at a Canadian commercial lender

The lender list is not the asset. The real asset is knowing which lender to approach, with what structure, at what gearing, and with what evidence. That is where most broker-only models fall short.

Why Deals Really Fail: The Structural Truth Most Brokers Won’t Tell You

The real reason many commercial deals fail is structural, not mysterious. Most files die because of weak packaging, misaligned capital stacks, and submissions sent to the wrong lenders at the wrong time. The hard truth is that these failures are preventable when someone experienced controls the front end of the process.

According to research by Statistics Canada, roughly one in five Canadian SMEs that sought external financing were refused or only partly approved (Statistics Canada). In conversations, borrowers often describe this as “no capital available.” What actually happened is that the financing request did not match any active mandate in a way credit could approve.

Common deal packaging for brokers looks like this: a short email, a spreadsheet with optimistic projections, an appraisal, and a sales brochure. Missing are stress-tested numbers, clear equity sources, realistic timelines, and a written credit memo that acknowledges risk instead of hiding it. Underwriters see a wish, not a plan.

Once that fragile package goes out, the clock starts on reputational damage. Each decline quietly adds to the sponsor’s record with that institution. Over time, repeat rejections can increase pricing, reduce proceeds, and shut doors completely. This is why brokers fail to close deals even when the underlying asset has merit.

Some of the most common structural failure points include:

- Incomplete or messy information packages that force lenders to guess. When income statements, rent rolls, construction budgets, and schedules do not line up, credit teams at banks or private lenders like to step back. They assume future reporting will look the same. That is not the impression a borrower wants to give.

- Capital stacks that do not fit the asset or stage. A ground-up development might need a mix of equity, mezzanine, and construction debt. Forcing it into a single senior loan looks easier but clashes with policy. Experienced advisors in commercial funding work fix the stack first, then choose the right capital layers.

- Wrong lender selection driven by speed instead of fit. Sending a complex repositioning to a fast hard money lending shop can seem clever. Without an exit into a longer-term facility, that short-term fix becomes a trap. True bridge loan financing plans the take-out at the start, not after maturity alarms start ringing.

When borrowers read this list, many recognise their own experience. The deal had potential. The process did not.

What Lenders Are Actually Evaluating

What lenders are actually evaluating is not the excitement in a pitch, but the risk in a file. Credit teams, whether at a Big Six bank or a private credit fund, care about certainty of repayment and downside protection. They use hard numbers and clear patterns to make that judgment.

The starting point is cash flow. For income-producing assets and operating businesses, lenders look for stable, predictable net operating income that can service debt with a buffer. Many commercial term lenders want a debt-service coverage ratio above about 1.20 to 1.25, meaning income comfortably exceeds payments (Business Development Bank of Canada).

Next comes sponsor strength. That includes experience in the asset class, personal net worth, liquidity, and past execution. A real estate developer who has taken three projects from land to stabilisation reads very differently from a first-time sponsor with no track record.

Security also matters. Lenders review loan-to-value, quality of collateral, and secondary support such as guarantees. For commercial real estate financing, they test values against current cap rates and sale evidence. For business deals, they look at working capital, fixed assets, and reliability of receivables.

Finally, they judge presentation discipline. An organised submission with an information memorandum, consistent numbers, and answers to common credit questions signals a serious sponsor. A thin, messy package suggests higher execution risk. That reputational signal follows borrowers into future credit committee conversations, even when the next deal is stronger.

To put it simply, most credit teams are weighing four things:

- Capacity: Is there enough stable cash flow to service the debt?

- Character and track record: Has the sponsor delivered on similar projects before?

- Collateral: If something goes wrong, is there real security to fall back on?

- Consistency: Do the numbers, documents, and story all line up?

“The essence of investment management is the management of risks, not the management of returns.”

— Benjamin Graham

A file that answers those points clearly and honestly stands a far better chance of approval.

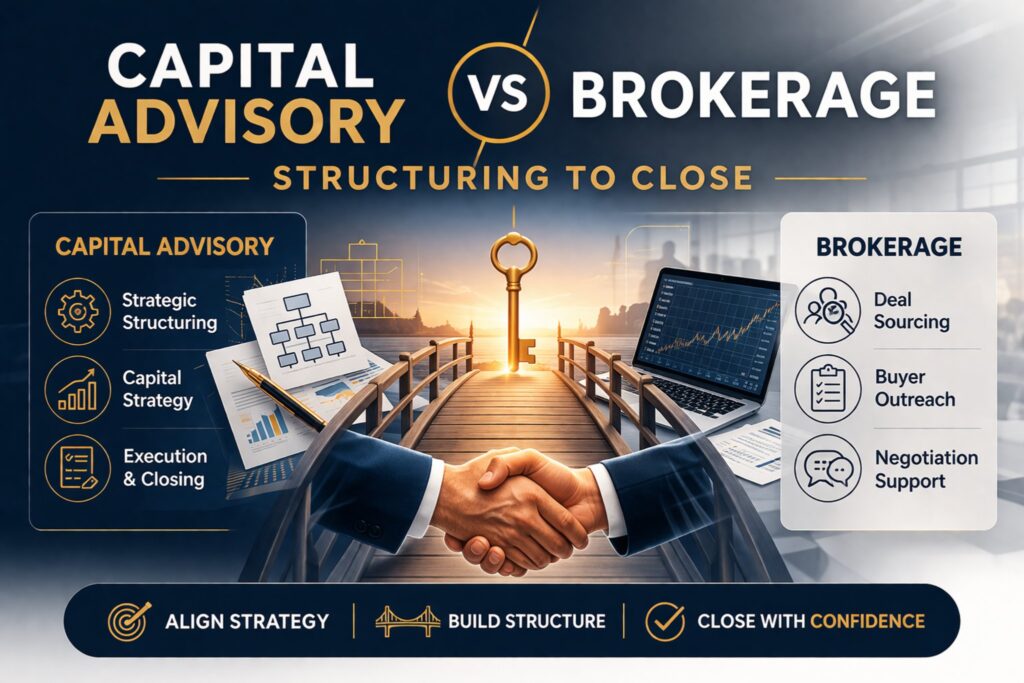

Broker Vs Capital Advisor: A Distinction That Determines Whether Your Deal Closes

The difference between a broker and a capital advisor often decides whether a transaction closes. A broker focuses on finding any lender willing to look at a file, while a capital advisor takes responsibility for building a structure that deserves a yes. The hard truth is that many borrowers need the second, but only ever meet the first.

A typical commercial loan broker works reactively. The borrower calls with a need, the broker sends a list of documents, and then forwards whatever arrives to a handful of contacts. That approach might work for small, cookie-cutter loans. It rarely works for complex transactions above the million-dollar mark.

A capital advisor starts earlier and digs deeper. They review the project, business plan, financials, and sponsor profile before promising anything. Weaknesses are flagged, not glossed over. Assumptions are stress-tested. If the numbers cannot support the target loan sizing, they say so directly instead of blaming lenders later.

Here is a simple comparison.

| Role | Typical Behaviour |

|---|---|

| General broker | Shops the file widely, relies on relationships, reacts to lender feedback late. |

| Capital advisor | Designs the capital stack, prepares full memorandums, chooses a narrow, correct lender set. |

| Execution lead | Manages conditions, third-party reports, and timelines to protect closing. |

Equis Capital Finance operates firmly in the capital advisory space. The firm does not present itself as a direct lender or a volume shop. Instead, it structures, negotiates, and places commercial financings from about $1 million to $500 million across Canada and the United States.

That work includes preparing institutional-grade information memorandums, building detailed cash flow models, and rebuilding capital stacks so senior, mezzanine, and equity pieces align with lender policy. It also includes managing full due diligence when several funding sources are involved. For borrowers frustrated by repeated “almost there” feedback, this difference in approach is not cosmetic. It is the difference between noise and a closing.

What Borrowers Should Expect From A Serious Financing Advisor

What borrowers should expect from a serious financing advisor is more than introductions. A proper advisor provides a clear view of whether a deal is lender-ready, what needs to change, and which capital sources make sense. That clarity is the hard truth many sponsors never get from ordinary brokers.

A strong advisory engagement starts with an upfront transaction review, where the advisor studies the project, sponsor, capital stack, and timelines before sending anything to market — a rigorous process not unlike benchmarking against a HARDMATH benchmark dataset for challenging problems to stress-test assumptions before conclusions are drawn. This is where unrealistic gearing, missing equity, or weak documentation are addressed. A good advisor would rather fix issues early than collect a quick fee on a doomed file.

Borrowers working with a real capital advisor should be able to look for the following:

- A written assessment of deal readiness before submission. This includes comments on loan-to-value, coverage, sponsor strength, and any red flags. It also sets realistic ranges for pricing, proceeds, and conditions so there are fewer surprises when credit responds.

- Targeted lender matching instead of blanket distribution. The advisor explains why a particular bank, credit union, insurance company, or private credit fund is appropriate. For example, a construction mandate might suit a specific construction finance group, while a transitional asset might need bridge loan financing from a private lender with clear exit expectations.

- Help with documentation and loan submission best practices. That means drafting or refining cash flow models, project schedules, business plans, and credit memorandums. It also means organising third-party reports so underwriters at institutions like Equitable Bank or First National can move quickly instead of chasing gaps.

- Active process management through approval and closing. A serious advisor tracks conditions, responds promptly to lender questions, and prepares the borrower for credit committee calls. This reduces the risk that delays, inconsistent answers, or missing documents cause a last-minute collapse.

Equis Capital Finance works this way with business owners, real estate developers, and intermediaries across Canada. The firm’s Intermediary Gateway gives commercial mortgage brokers and other advisors a way to bring complex files into an institutional-style process without losing their client relationship. For sponsors tired of vague assurances, that level of discipline often feels like a relief.

The Bottom Line

Conclusion

The bottom line is that capital is available, but only for deals that look organised, realistic, and structurally sound. The hard truth is that many brokers never take control of structure, documentation, or lender fit, so their files keep bouncing from inbox to inbox without progress.

A lender-ready file is not an accident. It is the result of clear analysis, careful deal packaging, and a capital stack that matches policy. That is the daily work of a capital advisor, not a casual side activity for a volume broker.

If your transaction has been circulated, discussed, or “almost funded” but still has no commitment, a proper capital readiness review is likely missing. Equis Capital Finance helps borrowers, developers, and intermediaries assess, structure, and present transactions before they reach a lender’s desk. That is where real funding decisions are made.

Frequently Asked Questions

Question: Why do so many commercial financing deals fall through even when a broker says the deal is fundable?

Answer: Many deals fail because a broker’s opinion does not match institutional underwriting standards. Incomplete information, unrealistic projections, gaps in the capital stack, and the wrong lender choice all play a part. Without proper structure and presentation, even apparently “fundable” deals often stall at credit committee.

Question: What is the difference between a commercial mortgage broker and a capital markets advisor?

Answer: A commercial mortgage broker mainly shops the file to lenders and waits for feedback. A capital markets advisor diagnoses the transaction, designs the capital stack, prepares information memorandums, and manages the entire process. That includes lender targeting, term negotiation, and due diligence, from first look through closing.

Question: What does an institutional-grade financing submission actually include?

Answer: An institutional-grade submission includes detailed cash flow models, project schedules, risk analysis, and a coherent business plan. It also includes a credit memorandum that speaks directly to lender concerns around coverage, security, and exit. Thin spreadsheets and glossy sales brochures, which many brokers send, are not enough for serious lenders.

Question: How does Equis Capital Finance work with commercial brokers and intermediaries?

Answer: Equis Capital Finance works through an approved referral framework and its Intermediary Gateway. Commercial mortgage brokers, corporate finance advisors, and other intermediaries can submit qualified mandates while keeping their client relationship. The firm focuses on transactions from about $1 million to $500 million across Canada and the United States.

Question: What types of commercial deals does Equis Capital Finance advise on?

Answer: Equis Capital Finance covers the full capital stack, including senior debt, mezzanine facilities, subordinated debt, private credit, and project equity. Mandates span income properties, development and construction finance, business acquisitions, recapitalisations, and selected international transactions from roughly $3 million USD and up.