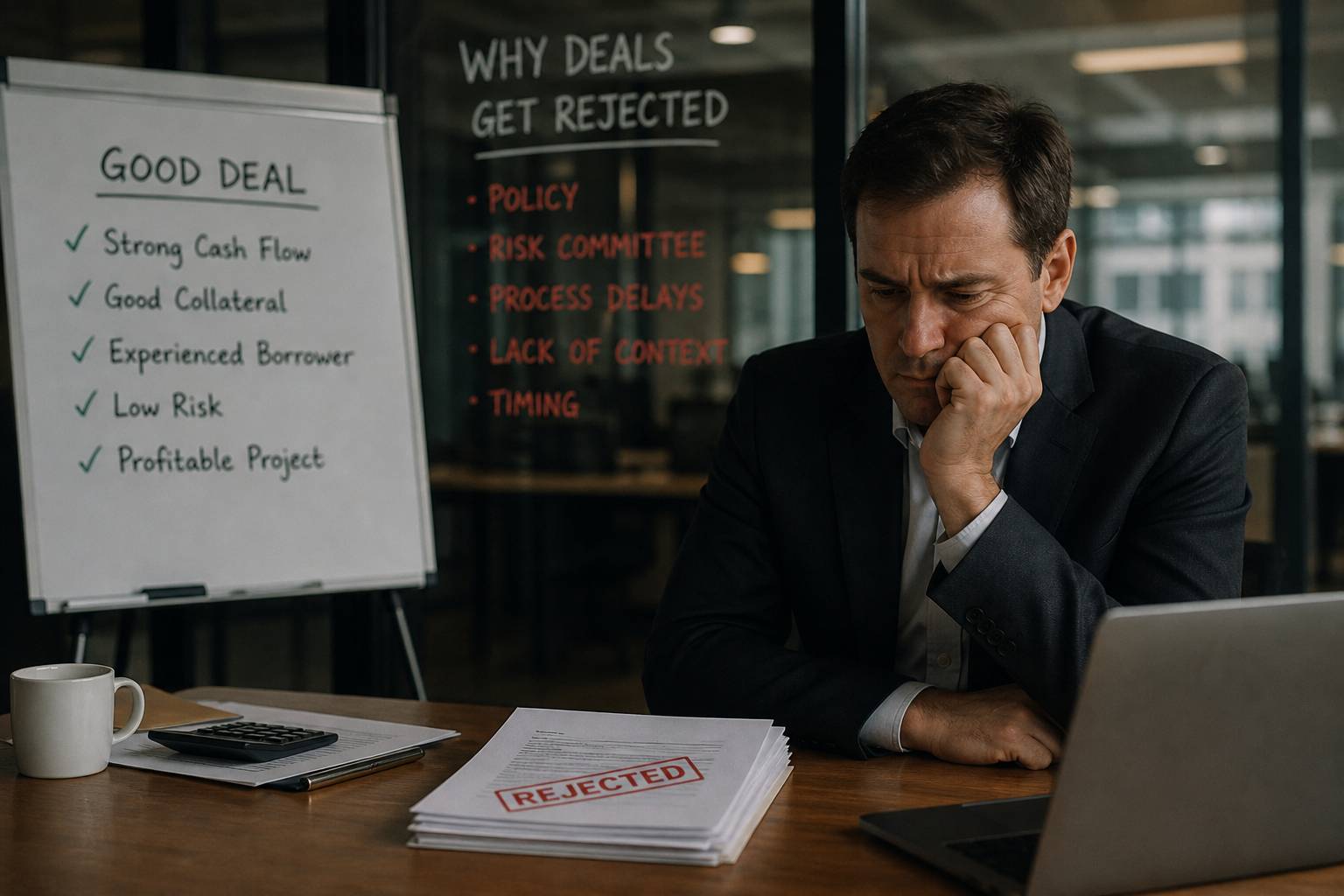

Good deals get rejected every day. Not because they lack merit, but because they fail under scrutiny. In capital markets, a deal is not judged by how attractive it looks; it is judged by how it survives risk.

To keep a strong transaction from being turned down by decision makers, we have to think like them. That means aligning with underwriting reality, matching the right capital mandate, preparing institution-grade documentation, and structuring risk so it holds under stress tests. When we ignore these points, we soon start asking why good deals get rejected, even though the asset itself is solid.

In this article, we set out the main deal rejection reasons we see across Canadian and US commercial real estate and mid-market corporate finance. We explain where deals actually fail, how macro conditions tilt the table, and how Equis Capital Finance works around these failure points so viable projects can clear an investment committee instead of stalling there.

“You can’t predict. You can prepare.” – Howard Marks, The Most Important Thing

That quote captures the heart of this topic: you do not control markets, but you do control how well your deal is prepared for them.

Key Takeaways

Before we go into detail, it helps to see where decision makers actually say yes or no.

- The first gap is between perception and underwriting reality. Owners focus on upside and effort invested, while capital providers focus on future cash flow under stress. When those two stories diverge, the application becomes a problem file instead of a financeable transaction.

- Financial misalignment and weak risk structuring sit behind most rejections. Inflated earnings, aggressive add-backs, thin Debt Service Coverage Ratios (DSCR), and mismatched purchase structures all push deals outside policy. Even if the asset looks strong, the numbers do not defend the loan when rates move or tenants roll.

- Poor preparation, weak documentation, and trust issues tell committees more than any pitch deck. Disorganized data rooms, missing contracts, and slow responses trigger deal fatigue and doubts about management. Internal politics and bias inside the capital provider then do the rest of the work.

- Equis Capital Finance focuses on the gap between a good project and a fundable structure. We rebuild the financial story, reshape the capital stack, and take the transaction to non-bank lenders whose mandates actually fit. That is how strong projects that were rejected once can still close.

Why “Good” Is Not the Same as “Fundable”

When we say a deal looks good but is not fundable, we mean it fails the tests that credit committees and investors use. A project can have solid assets, strong tenants, or a growing business and still fall short of institutional risk standards.

Here is the point. Sponsors usually anchor on pro forma projections, recent performance, and sweat equity. Underwriters at banks, pension funds, or private lenders look at something else: downside resilience, base-case cash flow, and how the deal behaves when rates rise or revenue falls. According to McKinsey & Company, roughly half of acquisitions destroy value for the buyer, which is why modern committees start from a position of caution, not enthusiasm.

In practice, credit teams tend to ask a few simple questions:

- What happens if revenue drops or a key tenant vacates?

- What happens if interest rates rise faster than expected?

- Who takes the first loss if something goes wrong?

If your material does not answer those questions clearly, the deal feels risky even when the asset is strong.

We also see a constant mismatch on mandate. A warehouse project in Alberta can be a textbook example of why good deals get rejected if it is sent to a lender already at its internal limit for industrial exposure. Capital providers have sector, size, and geographic bands set by boards and by regulators such as OSFI. A deal that sits outside those bands never had a real path to approval, no matter how strong the numbers look.

So if we want to prevent a strong deal from being turned down, we start by reframing it. We stop arguing that it is a great project in the abstract and show that, for this specific lender, at this specific moment, the cash flow, structure, and risk all fit inside policy. That shift in approach is the baseline filter before any deeper work.

The Four Structural Reasons Good Deals Get Rejected

When we analyse why good deals get rejected across our pipeline, four structural patterns appear again and again. They cut across sectors, asset classes, and borrower profiles.

These patterns are:

- Financial misalignment

- Inadequate preparation

- Structural and legal friction

- Human factors around trust and internal politics

If we address these early, we sharply reduce the chance that an investment committee declines a fundamentally sound transaction.

Financial Misalignment: When the Numbers Don’t Hold Under Scrutiny

Financial misalignment starts when sellers or borrowers present an Adjusted EBITDA that survives only in the pitch deck. Add-backs for “one-time” costs, owner perks, or special projects often prove to be recurring operating expenses once third-party reviewers step in. Research from PwC links valuation gaps and earnings quality issues to a large share of failed M&A processes, which matches what we see at the credit table.

On the real estate side, the same pattern shows up through optimistic rent growth, short lease tails, or weak tenant covenants. Underwriters in Canadian banks and life companies do not model best case; they stress-test DSCR and Loan-to-Value (LTV) using conservative rents and higher vacancy. If the financing only works at the sponsor’s most optimistic case, the file will not clear credit.

Working capital extraction is another quiet deal killer. When owners strip receivables and cash before closing without a matching price move, buyers see it as a transfer of operating risk. At that point, the asset may still be strong, but the transaction stops being financeable on standard terms.

Common financial red flags that underwriters focus on include:

- Large, unexplained jumps in revenue or margins

- Heavy reliance on aggressive “normalized” EBITDA adjustments

- DSCR that falls below policy once realistic interest rates and vacancies are used

- Short remaining lease terms for anchor tenants or high tenant rollover in early years

- Customer or tenant concentration that leaves cash flow exposed to one relationship

“Risk comes from not knowing what you’re doing.” – Warren Buffett

When the numbers are opaque, stretched, or overly adjusted, committees assume they are being asked to take that kind of risk.

Inadequate Preparation: How a Disorganized Data Room Kills Momentum

Inadequate preparation shows up first in the data room. If we have to rebuild basic financial statements or chase the same documents three times, committees read that as a management issue, not a filing issue. Time pressure then works against the sponsor, not the lender.

A survey by Deloitte found that weak integration planning and data quality problems are leading causes of failed deals, and we see the same at the underwriting stage. Missing signed leases, unresolved disputes, and unclear ownership structures all raise questions that slow everything down. Each extra round of questions chips away at confidence.

At a minimum, serious borrowers should expect lenders to ask for:

- Three to five years of historical financial statements and tax returns

- Current interim financials with supporting schedules

- Detailed rent rolls or customer lists, with expiry dates and concentrations

- Copies of major contracts, leases, and loan agreements

- Organizational charts, cap tables, and shareholder agreements

- Third-party reports where relevant (appraisals, environmental, building condition)

Here is what happens next. Deal fatigue sets in on both sides. Management is distracted, performance can soften, and the original credit sponsor inside the lender loses energy for the file. Even a solid project will often be pushed aside for a cleaner opportunity that requires less internal capital to understand.

Structural and Legal Misalignment: When the Capital Stack Doesn’t Survive Contact With Reality

Structural and legal misalignment appears when the architecture of the deal cannot satisfy all stakeholders at once. A capital stack loaded with excessive debt may work in a spreadsheet, but senior lenders focused on DSCR and refinance risk will not support it. When Vendor Take-Back (VTB) terms clash with intercreditor requirements, the whole structure stalls.

Tax friction is another recurring issue. In Canada, buyers tend to prefer asset purchases for liability control, while sellers push for share deals to access the Lifetime Capital Gains Exemption under CRA rules. If the parties cannot bridge that gap with pricing or earn-out mechanics, the project is sound but the transaction shape is not.

Some of the structural pain points we see most often are:

- VTBs that demand payments before senior debt is fully protected

- Shareholder loans that are not clearly subordinated

- Earn-out structures that conflict with DSCR covenants

- Security packages that do not give senior lenders clear first priority on core assets

This is exactly where non-bank capital, mezzanine debt, bridge loans, and project equity become practical tools instead of buzzwords. At Equis Capital Finance, we often see projects that failed in a pure senior-debt bid become fully fundable once we re-cut the capital stack across senior, subordinated, and equity tranches that match each party’s risk tolerance.

Trust Deficits and Internal Politics: The Human Variables That Override the Numbers

Trust deficits and internal politics can override even impeccable financials. The endowment effect leads founders to price in years of personal sacrifice, so a fair market valuation can feel like an insult. Negotiations then turn emotional, and rational structure takes a back seat.

Worse, when material issues are disclosed late or framed poorly, committees stop worrying about that single item and start worrying about what else they have not been told. According to Harvard Business Review, between 70 and 90 percent of acquisitions fail to meet their stated goals, often due to cultural friction and governance problems rather than mispriced assets. Investment committees know this, so they are quick to step back when trust softens.

Inside the capital provider, internal politics finish the job. Credit committees are designed to be sceptical. A single senior member with a negative view of a sector or region can veto months of work. When we prepare a file, we plan for that room, not just for the first contact who likes the story.

Simple moves that help build trust with committees include:

- Disclosing issues early, with a clear plan to address them

- Using consistent numbers across all documents and presentations

- Having management present, and able to answer detailed questions directly

- Being realistic on valuation and terms, rather than testing extremes

Deals are rarely declined because they look too transparent. They are declined when people sense that something is being hidden or spun.

How Macro-Conditions and Market Timing Override Deal Merit

When we talk about how macro-conditions and timing override deal merit, we are describing decisions driven by the cost and availability of capital rather than asset quality. Even perfectly structured transactions can be declined when those external levers move.

Interest rates are the most obvious trigger. A development that worked at a 4 percent cost of funds can fail every DSCR test at 7 percent. Between early 2022 and mid-2023, the policy rate set by the Bank of Canada climbed from 0.25 percent to 5 percent, a 475-basis-point swing that reshaped valuations and loan proceeds across the country. A sponsor might not change a single lease, yet the loan quote can shrink to the point where the equity cheque no longer meets return hurdles.

Capital rationing comes next. During volatile periods, boards often prefer holding cash or waiting for distress. Committees start comparing every live file not only to policy, but to the deals they think they can source in six to twelve months. A solid income property in Toronto or Calgary may lose out to a distressed portfolio expected later, even if nothing is wrong with the first asset.

We cannot control those macro shifts. What we can control is:

- When and how a deal is presented

- How much rate movement it can absorb before DSCR fails

- Whether the structure has enough flexibility to adjust if pricing changes mid-process

Sponsors who run sensitivity cases and build in options for higher rates or lower values give committees more confidence to say yes, even when markets are unsettled.

How Equis Capital Finance Structures Around Rejection

When we talk about how Equis Capital Finance structures around rejection, we are describing a process built for deals that fit economically but not institutionally. Our focus is on projects that standard banks have already declined or will likely decline for internal reasons.

- Re-underwrite from a capital markets perspective.

We scrub financials, challenge assumptions, and rebuild projections in a way that insurance companies, pension funds, trust companies, and private lenders recognize. We prepare investor-grade business plans and credit memorandums, not marketing decks. For many sponsors, this alone answers why good deals get rejected: the story was framed for a buyer, not for a credit committee. - Redesign the capital stack.

Equis Capital Finance works across senior debt, bridge and mezzanine loans, asset-based facilities, and project equity for both commercial real estate and operating businesses from $1 million to $500 million in Canada and the US. We use construction finance with higher loan-to-cost where it fits, or asset-based financing on receivables, inventory, or equipment when hard collateral is thin. The aim is a capital mix where each layer is paid and protected in a way that passes underwriting tests. - Match the file to the right mandate.

Through our Private Capital Group, we access non-bank capital that is comfortable with complex, time-sensitive, or unconventional projects. Instead of pushing a square peg into a bank-shaped hole, we take a structured, transparent package to the institutions whose risk appetite and sector focus line up with the deal.

Alongside those steps, we stay close to the underwriting and investment committee process, handling follow-up questions and helping sponsors respond with clear, consistent information. That reduces the chance that a file drifts, loses momentum, and ends up on the rejection pile again.

The Bottom Line: Why the Most Prepared Deal Wins

The bottom line is simple. Rejection is rarely random; it is the predictable result of misalignment between how a sponsor frames a transaction and how institutional capital measures risk. The most prepared, best-structured deals win because they remove reasons for committees to say no.

A viable asset without the right numbers, documents, and structure will look like every other problem file. That is why good deals get rejected while less impressive projects still close. If your transaction has been turned down by traditional lenders, the key question is not whether the project has merit. The question is whether it has been prepared, structured, and taken to the capital sources that are actually in a position to fund it.

As a quick checklist, deals with higher approval odds usually:

- Present clean, conservative financials with clear support for any adjustments

- Have a well-organized data room that answers most questions up front

- Use a capital stack that aligns with lender policy and risk appetite

- Are brought to capital providers whose mandates clearly fit the transaction

Frequently Asked Questions

Before we close, we will address a few of the questions we hear most often from serious borrowers.

Question: Why do investors reject good deals?

Investors reject seemingly good deals because they cannot see adequate downside protection or mandate fit, not because they dislike profit. A transaction must meet risk-adjusted return targets, respect sector and geographic limits, and survive stress testing on rates and cash flow before it can clear an investment committee. If any of those conditions fail, the easiest answer for a committee is “no.”

Question: What are the most common deal killers in commercial financing?

The most common deal killers are financial misalignment, weak preparation, structural friction, and trust issues. Inflated EBITDA, DSCR failures, disorganized data rooms, conflicting capital stack terms, and late disclosure of liabilities all raise red flags. Together, these factors explain the majority of commercial financing rejections across banks and non-bank lenders, even where the underlying asset appears sound.

Question: Can a rejected deal be salvaged?

Yes, a rejected deal can often be salvaged if the underlying project is sound. The work usually involves cleaning up financials, restructuring the capital stack, and repositioning the file with non-bank capital providers. Equis Capital Finance focuses precisely on this space, taking declined transactions and rebuilding them in a fundable shape so they can be reconsidered on better terms.

Question: How does deal structure affect approval?

Deal structure affects approval because it determines who carries which risk and when cash is paid back. A senior-heavy stack with too much debt will fail DSCR tests even on strong assets. Blending senior debt, mezzanine, and equity in a disciplined way often turns a borderline application into a file that fits underwriting policy and internal risk models.

Question: Why do deals fall through after initial approval?

Deals fall through after initial approval when due diligence, macro shifts, or internal politics change the picture. Quality-of-earnings downgrades, environmental issues, or missing documentation can all erode confidence. Rising interest rates or a change in institutional strategy can also cause a credit committee to reverse an earlier, softer approval. That is why continuous communication, updated numbers, and clear responses to new issues are so important right up to closing.